The end of the year approaches. Time to assess progress and get ready for a fresh start and new year. NOW is the time to clean up your accounting messes. Like being physically fit, fiscal fitness requires a bit of focus and discipline. The numbers may not be way off. So you and your accountant may be letting things slide. My encouragement: Clean it up. Commit to your fiscal fitness. Here are just a few reasons why…

- If the dollar amount is wrong, it may be way off in both directions. The net effect could be small but the data is unreliable. Better to trust every account, every dollar amount, on the reports.

- Someone may be pulling a fast one, counting on the fact that you don’t really know what the balances should be. This is how you get ripped off.

- Messy accounting is poor financial stewardship. It’s your money and your responsibility. Treat your assets respectfully if you want to grow them.

- When the books are right, your company is worth more when you go to sell it someday. Just saying.

So, here are some tips for fixing weird accounting entries…

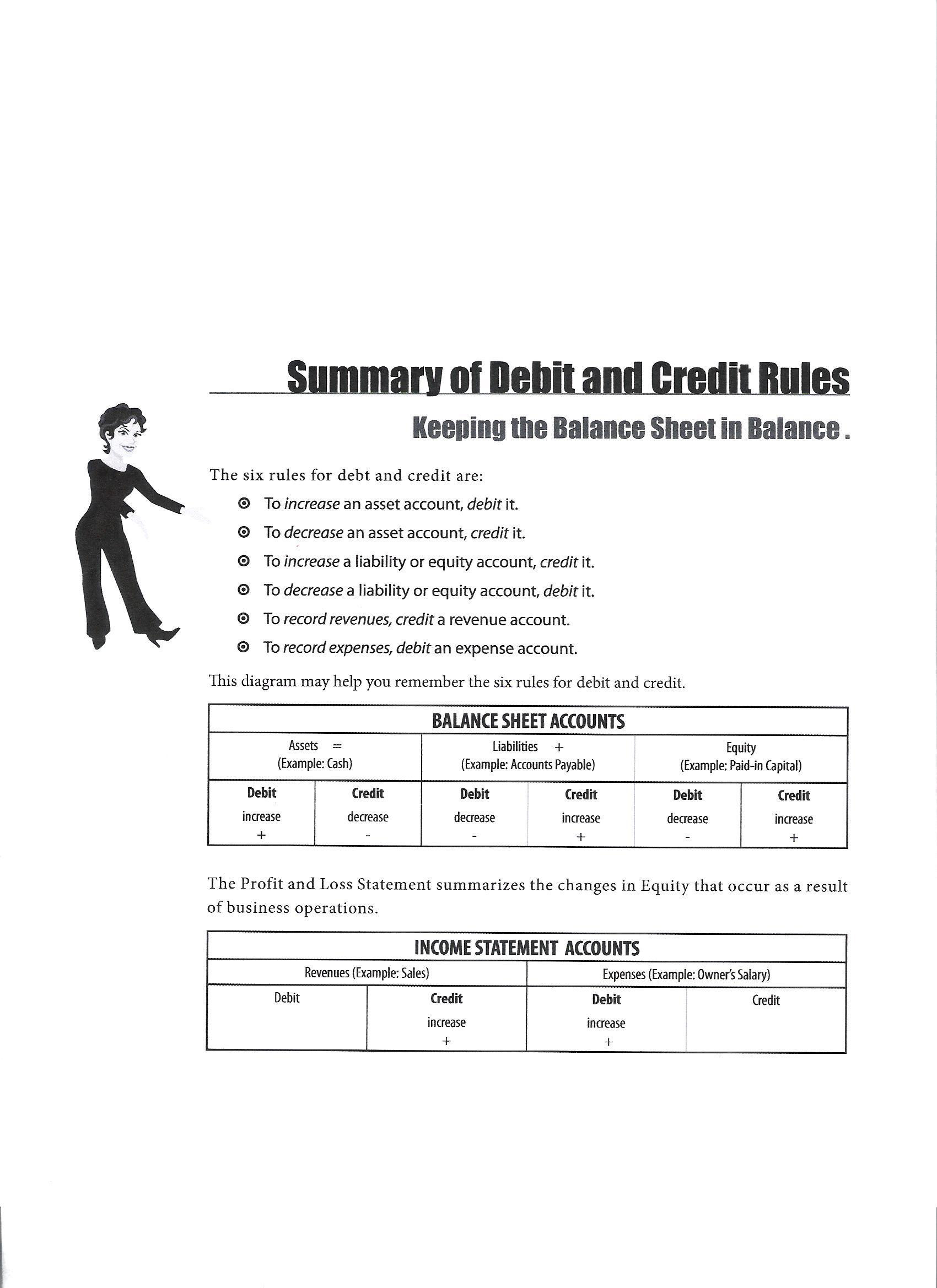

- Comb through every account on your Balance Sheet. Assets are what you HAVE. Every account is verifiable. Your Cash account should reflect what you actually have in that checking account. You can verify it by reconciling the account with your bank statement. Your Accounts Receivable account should total the dollar amount that you have billed customers but not yet been paid for. You can add up the stack of entered by not yet paid invoices. Liabilities – what you OWE – can be verified by the loan statements or credit card statements. Equity is the difference between Assets and Liabilities. Each account should be right. If it isn’t right, you have to adjust it to right.

- Use Journal Entries – Debits and Credits – to get the balances right. Suppose the Asset account for Inventory says that you have $$75,000 in Inventory. But you counted your Inventory and your actually have $55,000 worth of stuff on the shelves and in the trucks. Credit Inventory $20,000 and Debit COGS Materials $20,000.

- The fix gets a little trickier if it involves a “linked” account. For instance, if your AR balance reflects a weird balances, you can’t use a Journal Entry to fix AR. You have to find the customer account that is creating the weird balance. Make an adjustment to the customer’s account…to make it right. If they customer doesn’t owe you anything, adjust the account to zero. Code the entry to Sales or an expense called Adjustment. Leave lots of notes in the description fields. If the discrepancy is less than $1000, and has been hanging around your reports for 10 years, make the fix. Bottom line, the accounts have to be right.

- Run the Balance Sheet before and after the fix. Look for the effect, the Debit and Credit, of your adjustment. Verify…are the accounts right? Bit by bit, clean it up.

- Then, write procedures to make sure the data is being entered properly. Most importantly, starting now, review the Balance Sheet weekly so you find and fix mistakes quickly, before they become old, stinky, weird accounting entries.

- Work with your accountant and bookkeeper to drill into each account and fix the balances. Your accountant can let you know if the weirdnesses are big enough to justify an amended tax return. Chances are good that you can just fix them. Keep a journal of your fixes.

- If you ever get audited, show the auditor what you did. Say, “There were some weird accounting entries. At year end 2014, I reviewed every account and adjusted them to right. Here are notes about what I did. Some of the stuff we fixed was left over from entries going back to 2008. I really didn’t know much about accounting and finance back then. I’ve gotten smarter. The books are in good shape now.” Then, offer coffee and a snack and provide anything else the auditor asks for.

- Lighten up. Dig in. Learn something. This clean up can be kind of fun, like a Sudoku. Embrace the process. Do it now, so you don’t have to deal with the weirdness in 2015.

Join me for my next LIVE Online Workshop! The “Let’s Get Fiscal! Year End Accounting Wrap Up.” I’ve got lots more tips and tricks to fix stuff. We will work in real time so bring your weirdest accounting questions to the Workshop. I’ll keep it light and easy…and maintain your privacy, too. Get the books right and finish strong in 2014. Then, make 2015 your best year yet! Here’s the scoop for the Workshop…

{kind=link}